Mar 26, 2016

Why Investors Should HOPE the Market Goes Down

Written By: Nate Williams

Bring on the next recession!

The beginning of 2016 tested investors with the S&P 500 falling 10.51% in just over a month, hitting a low of 1,810.10 on February 11. Since that time, the US Market Index has pulled back, almost breaking even with the January 1, 2016 starting point of 2,043.94 with a closing price on March 16, 2016 of 2,027.22. At this point, most investors are wiping the sweat off their brow, breathing a sigh of relief and saying “that was close.”

During this volatile time period many of our clients called with concerns over the market decline. After recommending a new investing savings plan, one client texted me saying, “Looked at Schwab account last night…down $15,000…doesn’t make me want to jump into putting more money into stocks.”

My response was simple: “When the market falls you should be more excited to buy ownership of companies, not less excited!” Fortunately for him, and to his credit, he is a very coachable client. His response: “OK. Excited then.”

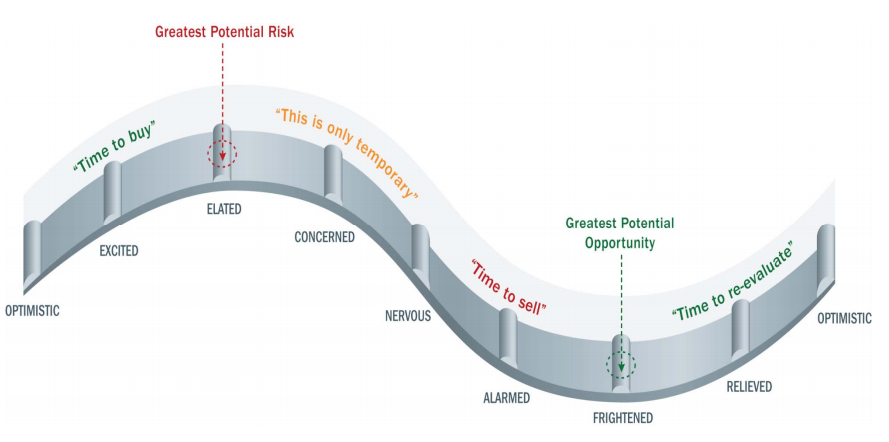

What about you? How do you feel when the market falls? If you’re like most people, your feelings are represented by this graph, with the grey line showing market prices:

As a living human, it’s normal to have “feelings” of concern when the market falls. But are those feelings rational? And do they align with what you should do and feel?

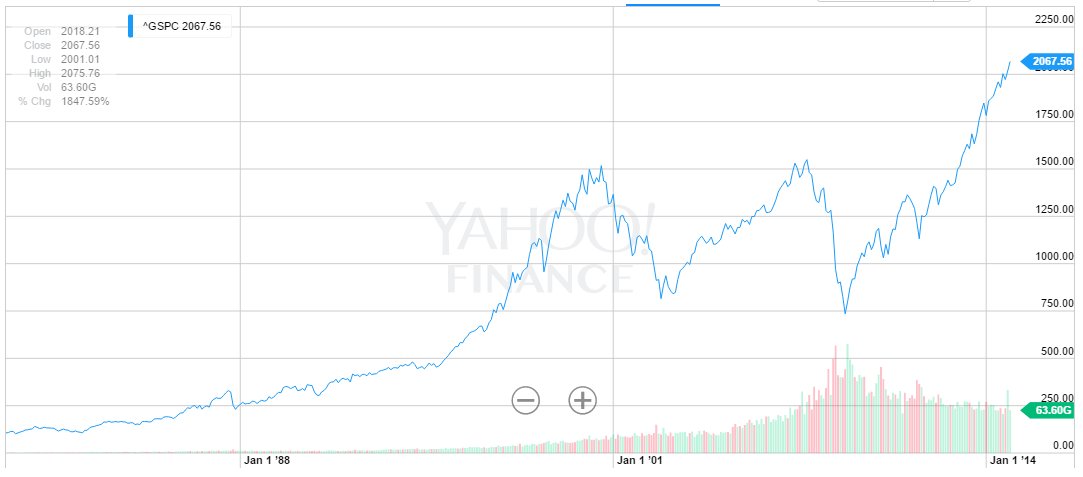

Try this little exercise: Look at the graph below of the US Market (S&P 500) over the past 30 years. Let’s assume you had money to invest all along the way. When do you wish you would have invested your money?

If you can do math and you’re not blind, you would have wanted to invest when the market is at its low points, right? As for me, I’m going all in on February 1, 2009!

But what were the vast majority of investors doing in Feb 2009? Including most professional money managers? They were running to cash, locking in losses forever!

Consider this quotes by the greatest investor of all time, Mr. Warren Buffett, in his 1997 letter to shareholders of Berkshire Hathaway:

“A short quiz: If you plan to eat hamburgers throughout your life and are not a cattle producer, should you wish for higher or lower prices for beef? Likewise, if you are going to buy a car from time to time but are not an auto manufacturer, should you prefer higher or lower car prices? These questions, of course, answer themselves.

But now for the final exam: If you expect to be a net saver during the next five years, should you hope for a higher or lower stock market during that period? Many investors get this one wrong. Even though they are going to be net buyers of stocks for many years to come, they are elated when stock prices rise and depressed when they fall. In effect, they rejoice because prices have risen for the “hamburgers” they will soon be buying. This reaction makes no sense. Only those who will be sellers of equities in the near future should be happy at seeing stocks rise. Prospective purchasers should much prefer sinking prices.”

So why does this happen – we get upset when the market falls, excited when the market climbs – time and again? We all know the drill, right? We all know that the market will ebb and flow; when it ebbs, again, why do we freak out? Why do we like paying more for burgers?!

I don’t know all the reasons for all people, but I think for most doctors the problem is centered around two key misunderstandings:

- Misunderstanding of what you own

- Misunderstanding of the plan

First, a misunderstanding of what you own. Here is a test: imagine you have a diversified portfolio of stocks (ownership of real companies) that was valued at $100,000 yesterday, but today the market tanks and the portfolio is now valued at only $80,000, how much have you lost? This is not a trick question. How much?

Most people will say $20,000, right? Well, those people are wrong. You haven’t lost anything. “Then it’s a trick,” you say. No, it’s not. Let’s assume in that portfolio you don’t hold any cash. Because cash is the commonly accepted method of trade, it’s the best and only way we have to show the current trading value of an asset. But it’s not the asset!

To be more specific, let’s assume you owned 1,000 shares of Apple stock, each valued at $100. And the next day the price per share drops to $80 – how much have you lost? Nothing. You still own 100 shares of Apple stock. Likewise, if the price increases to $120, what have you gained? Likewise, nothing. You only gain or lose money when you sell (you also gain when you earn interest or dividends that are reinvested).

The second problem, I think, is a misunderstanding of your real, long-term financial plan and the role that stocks play in that plan. Most doctors think the goal is to buy a bunch of stocks, hope the price goes up, and then sell them all on one magical day in retirement. This could happen, but for your sake I hope it doesn’t.

Don’t worry, most dental CPAs don’t get this point either. And neither do most investment advisors. So what is the plan?

Let’s pretend that you are a dentist in Phoenix, AZ, and that your financial plan is to buy as many single-family homes as possible during your working years (i.e. you buy “stock” in houses, read more here). After you buy the homes, your plan is to rent them out and one day you are going to stop practicing as a dentist and you’re going to live off the income from those properties. Got it? Now let me ask you a few questions:

- What will the rental rates (r) be in Phoenix in the year 2045 when you retire? You have no idea – you do believe, however, that there will be people living in Phoenix and those people will need a place to live.

- If you want to increase your income, what is the only guaranteed way to do that? Simple. Buy more houses. 2r is twice as much money as 1r, right?

- If your goal is to buy more houses, what do you hope happens to the price of houses in Phoenix during your working and buying years?

The answer to the last question is simple: you want the real estate market in Phoenix to tank! Please, bring back 2008! Why? Because in that year the cost of homes in Phoenix went down by over 50%! And so you could buy two for the price of one, effectively doubling the quality of your retirement!

So what does this have to do with your plan? Everything. This is your plan (sub stock and bond mutual funds for single-family homes, which are actually horrible investments for doctors). Your financial plan (assuming you have one, and that it’s a good one), is not to buy a bunch of stocks and then sell them on some special day when you turn 60 or 65. Your plan is to buy as many shares of stocks and bonds as possible (via mutual funds), then to live off the income from those companies for as long as possible (dividends, interest, etc.).

And if that is the goal, and it is, and if you’re in the phase in life when you’re buying not selling, then you’d be smart to pray for a market crash and rejoice when it comes.

Or to quote Warren Buffett, “Smile when you read a headline that says ‘Investors lose as market falls.’ Edit it in your mind to ‘Disinvestors lose as market falls – but investors gain.’” (http://www.berkshirehathaway.com/letters/1997.html)